Insight | The sky’s the limit

If you work in ancillary revenue for an airline, life is about to get very interesting. There’s a massive opportunity that’s set to take off – enabled by inflight broadband – and airlines are in the pilot’s seat. Up until now, the full scope hasn’t been realised, but the release of a new London School of Economics study reveals a market at the tipping point of transformation.

As we know, ancillary revenue is a lifeline for airlines, particularly at a time when seat margins are dwindling. Generated by everything from affiliated car hire and hotel bookings, to baggage fees and inflight retail, this additional income was estimated at $67.4bn in 2016 – 9% of global airline revenue, and the figure is set to double by 2020.

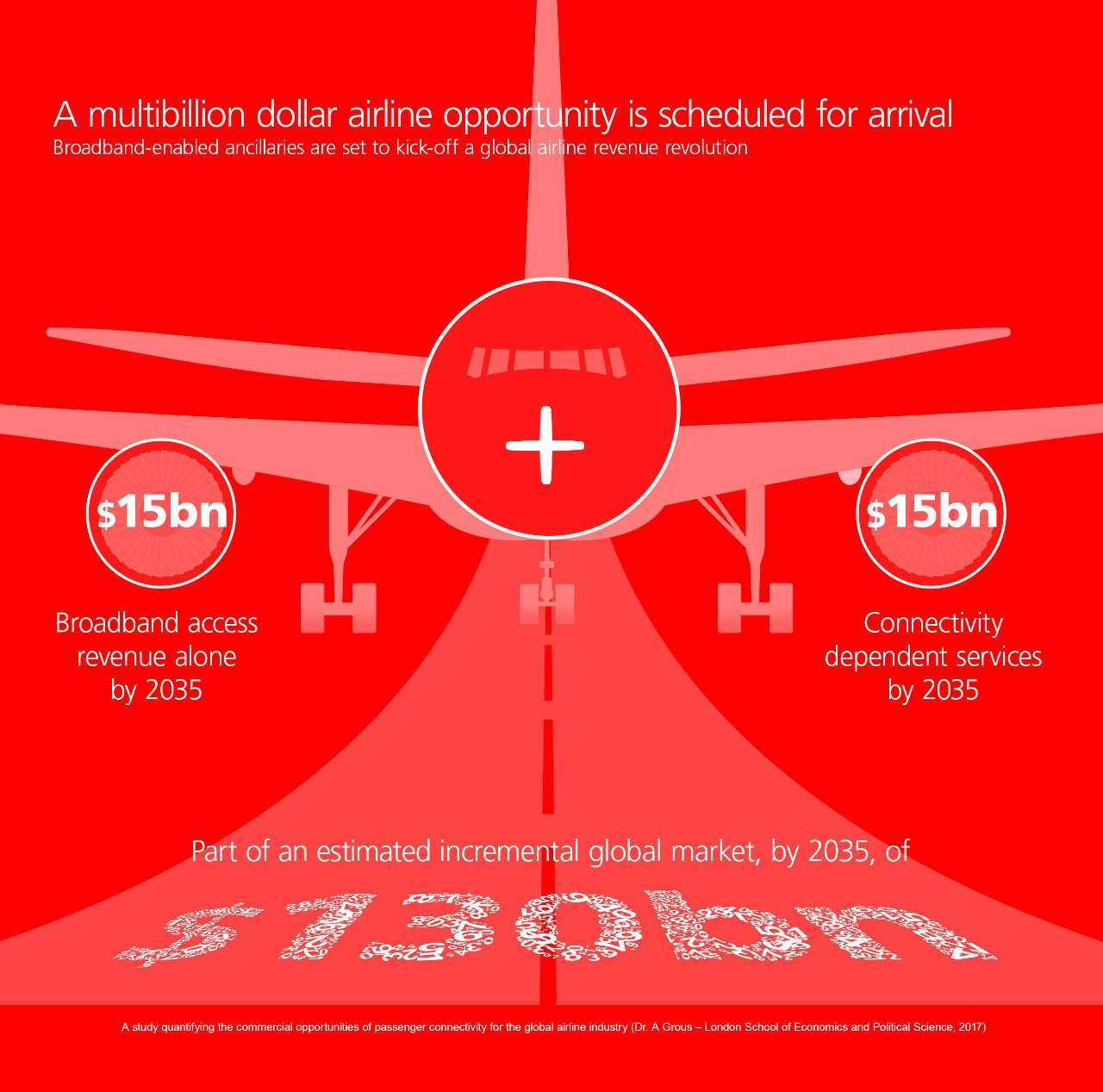

But the potential is forecast to be even greater, according to this ground-breaking LSE study – the result of over six months of detailed research and analysis. Thanks to the implementation of next-generation inflight broadband there’s a potential additional incremental opportunity of up to $30bn for the airline industry by 2035. So where’s that boost to the bottom line coming from?

Authored by Dr Alexander Grous of the LSE’s Department of Media and Communications, the study – Sky High Economics – is comprised of three chapters and it’s the first to comprehensively and independently assess the socio-economic impact of the inflight broadband revolution.

Chapter one, “Quantifying the Commercial Opportunities of Passenger Connectivity for the Global Airline Industry”, draws from a wide range of industry sources across six regions. Spanning North America, Latin America, Asia Pacific, Europe, Africa and the Middle East, these include passenger traffic data and growth forecasts from IATA and other industry sources, passenger trends, and terrestrial connectivity models and behaviours.

“This study builds on the work we’ve been doing in this area over the last couple of years and consolidates the global picture for the value of inflight broadband-enabled revenue,” says Dr Grous. “By bridging the gap between market estimates of ancillary revenue from current traditional sources and incremental revenue from broadband-enabled cabins, this first chapter gives airlines robust forecasts of market potential to inform their business models.”

"This first chapter gives the global picture for the value of inflight broadband-enabled revenue, giving airlines robust forecasts of market potential to inform their business models"

But if Wi-Fi in the sky has been around for a while, why has it taken so long to realise the range of previously untapped ancillary revenue opportunities?

The problem has been that with existing legacy technology often falling short on reliability, speed or coverage, and only 25% of commercial aircraft currently offering inflight connectivity of any kind, airlines haven’t yet capitalised on the true financial potential for the 3.8bn passengers who fly each year.

This goes some way to explain why broadband-enabled ancillary revenue is forecast to be a mere $900m in 2018 – a drop in the ocean compared to existing revenue from ‘traditional’ ancillary sources.

"The study highlights that quality of experience is the most requested aspect of mobile broadband"

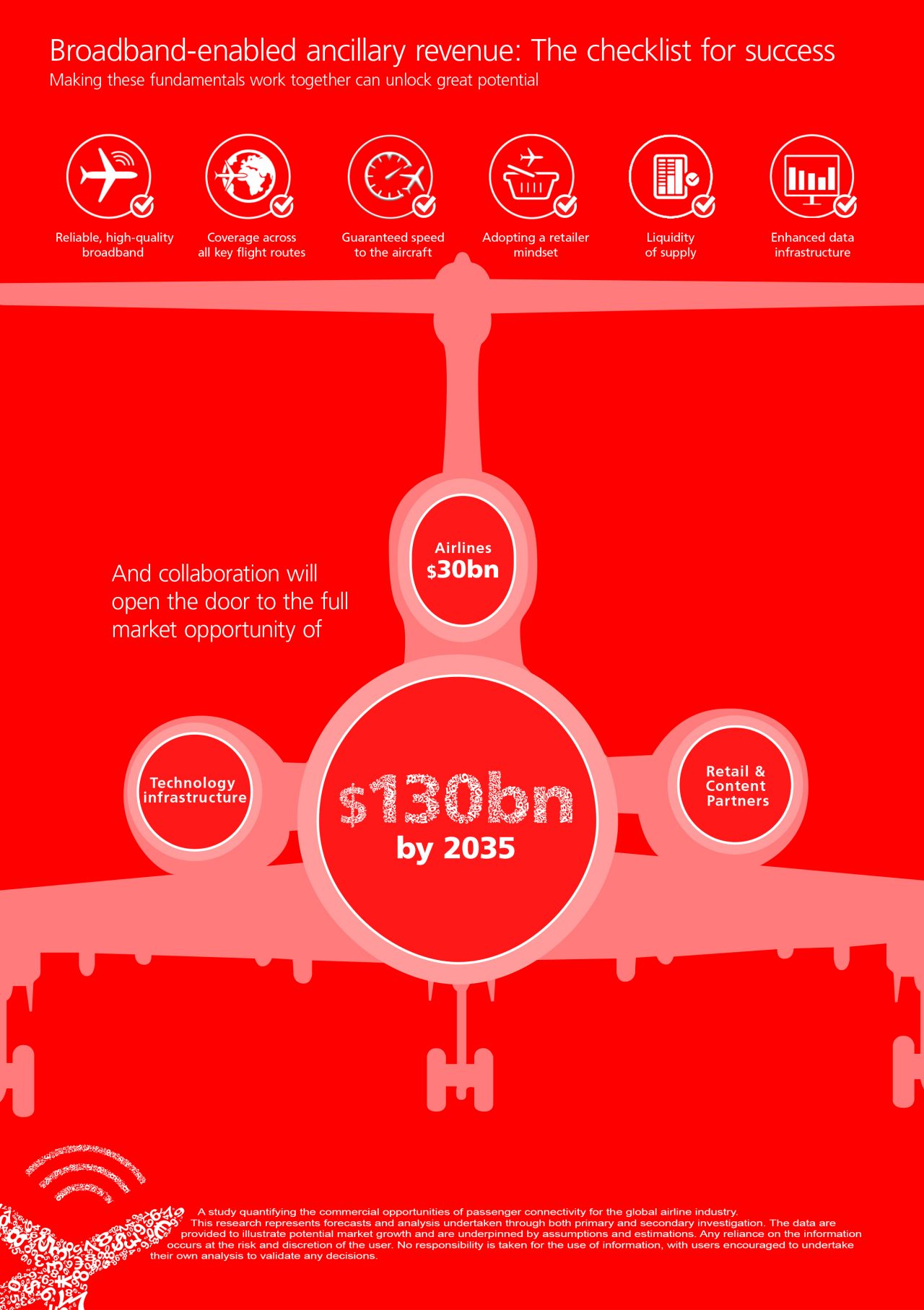

The study identifies six ‘preconditions of success’ which will allow ancillary broadband revenue to meet its potential. The first three of these are to do with technology and quality of service. Almost 80% of consumers experience mobile connectivity issues on the ground, including unreliability, slower-than-advertised speeds and inadequate coverage, and all have a knock-on effect for retention rates. The same is true in the air, where quality of experience is the number one driver. The report points to reliability, coverage of all flight routes and a guaranteed data speed to the aircraft as the essential foundations for the connected-ancillary revolution.

The study emphasises that when inflight broadband meets or exceeds passenger expectations, it can result in greater loyalty, which in turn can deliver a 23% premium over the average customer in profitability and revenue. So, with demand for mobile data increasing dramatically (18-fold in the five years from 2011, and forecast to represent 20% of all internet traffic by 2021) the opportunities to maximise the return on investment through a higher net present-value-per-passenger are evident.

Not that ubiquitous high-quality inflight broadband alone is enough to fully monetise this market.

Historically, the industry has tended to focus on seat-value rather than passenger value, but this is set to change. Airlines that continue to develop a retailer mind-set, delivering the right services and products to a passenger at the right time, will be the ones reaping the biggest rewards.

So it follows that making better use of the exceptional passenger data airlines already possess to create a single, accessible view of those individuals is an important driver too. Even today, only 11% of existing airline schemes offer personalised rewards based on purchase history or location data, despite evidence that the average order value for personalised transactions is 12% higher than those without.

Finally, to ensure the entire ecosystem can operate, airlines need to ensure ‘liquidity’ – sufficiently wide availability of products, content and services to give passengers the confidence to make purchases on board, or even postpone them until boarding. The study found that 85% of passengers can be influenced to make a purchase in a connected cabin if they can be sure the products they want will be available. With almost 5% of tour and 40% of entertainment bookings now made online and 65% of travellers booking hotels with mobile devices for same-day stays, these areas alone present airlines with an opportunity to capture revenue that’s otherwise largely out of reach. As the market develops and passengers become used to the availability of inflight connected services, their behaviours will change. For example, delaying a car hire booking until they are in flight, in order to get the best last-minute deal.

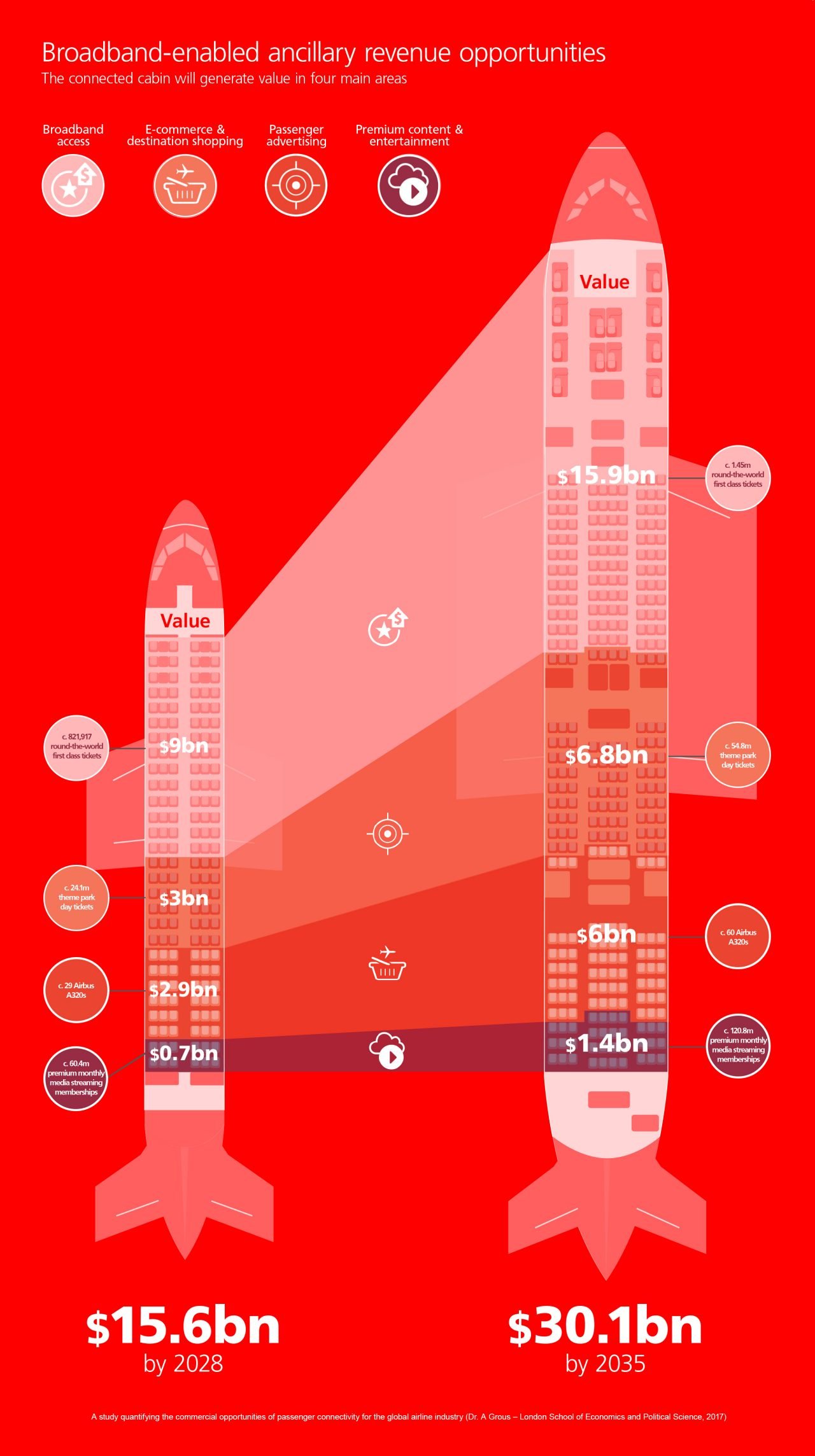

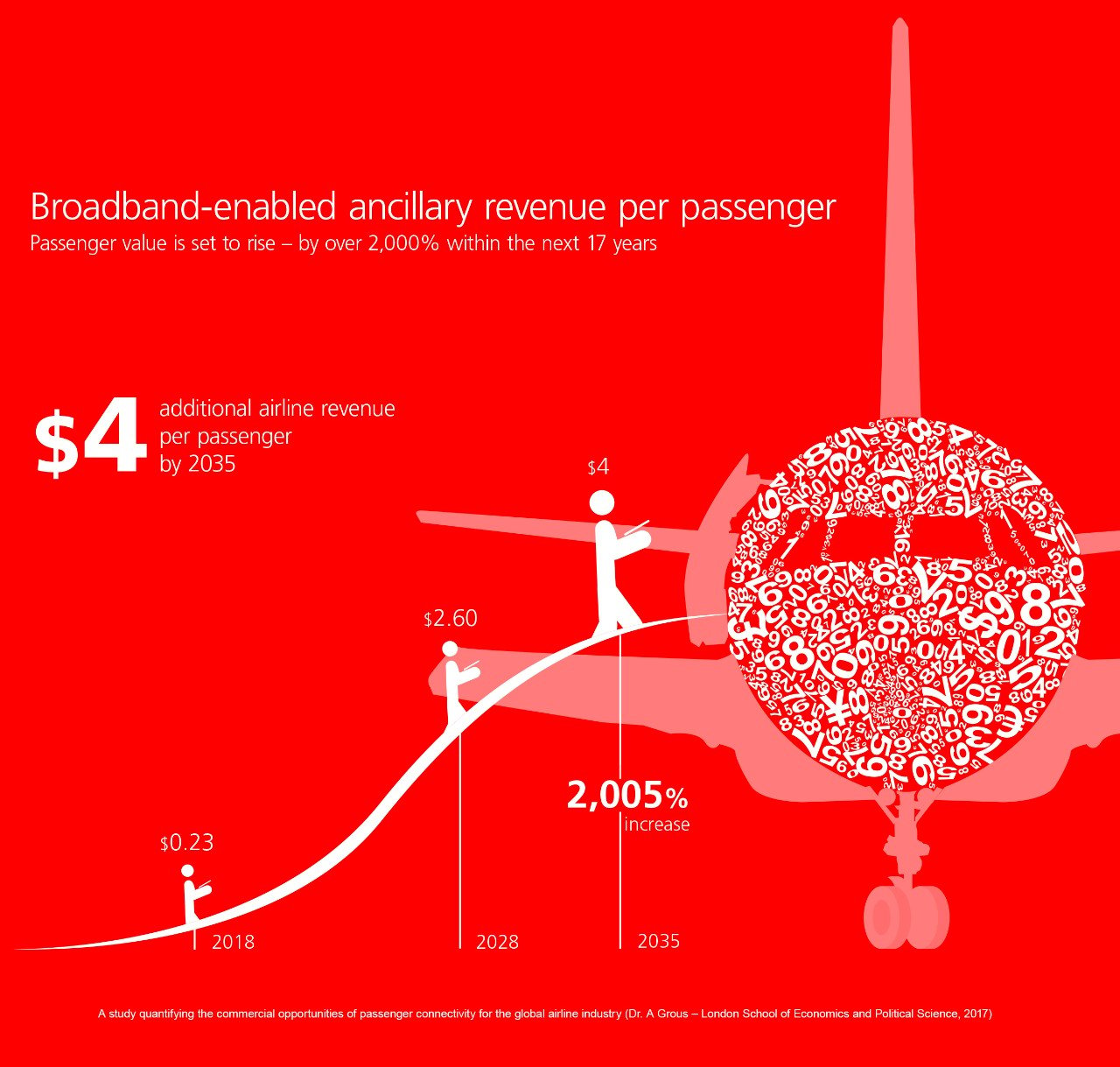

By 2035, broadband-enabled ancillary revenue of $30bn amounts to an average of $4 per passenger – a 2,005% increase on the $0.23 forecast for 2018. So how will that new revenue be generated? Sky High Economics identifies four main opportunities.

Access fees are already the largest source of broadband-enabled ancillary revenue and are forecast to remain so, but their contribution to the whole is expected to shift over time. So, while paying for inflight broadband is set to constitute 89% of broadband-enabled revenue in 2018, that share is forecast to decrease to 53% by 2035 as other streams mature. Regardless, that’s still a sizeable $15.9bn.

Inflight shopping is another area ripe for revolution. While revenue forecasts for broadband-enabled e-commerce today are a comparatively modest $36m, this opportunity is estimated to account for $6.8bn by 2035 – 22% of airlines’ total broadband-enabled revenue. Passengers will grow to be increasingly comfortable browsing online catalogues for inflight shopping – catalogues with items impractical to carry on board, and whose sale isn’t limited only to when the tax-free trolley passes down the aisle.

Airline passengers also present a captive market for discounted ‘late inventory’ that’s ripe for greater monetisation mid-flight. These short-dated items, such as car hire, hotel bookings and event tickets, generate zero return if not sold by a specific time and their last-minute nature make deep discounts viable – and targeted, personalised offers could make purchases even more tempting.

"Passengers present a captive market for discounted ‘late inventory’"

Advertising is also forecast to be an increasingly important source of broadband-enabled ancillary revenue. Online advertising is already widely accepted on the ground and terrestrial models can also be applied to monetise online content in the air (see article p9).

The study identifies three main areas of incremental revenue from broadband-enabled advertising inflight; from pay-per-click and the impression-based approaches typical of online advertising, to the interruption model that encourages audiences to pay a premium for ad-free services, to the broader opportunities of sponsored services.

The study makes conservative estimates for initial growth here, to reflect the technical aspects that need to be in place to accurately assign revenue while travelling. However, a captive audience could offer a higher level of engagement than on the ground, and the forecast is that overall advertising revenue could reach $6.1bn

by 2035.

In line with trends for the growth of streaming content services on the ground, revenue from access to premium entertainment content in the sky is forecast to reach $1.4bn by 2035.

The study suggests three primary models to monetise premium content. The first is live entertainment, such as sports events or news. The second involves premium on-demand content not already available via the IFE system – streamed to the aircraft rather than already installed on it, supplementing the existing entertainment offering (see article p40).

The final model Dr Grous highlights is W-IFEC bundling, where IFC purchase is a precondition to access premium streamed entertainment on BYOD devices. An ideal model for short haul carriers without embedded IFE systems.

As Sky High Economics explains, ancillary revenue from inflight broadband-enabled services may be in its early stages today, but, with IATA forecasting that passenger numbers worldwide will double to 7.2bn annually by 2035, there is huge potential for the industry, with new revenue opportunities for all airline business models.

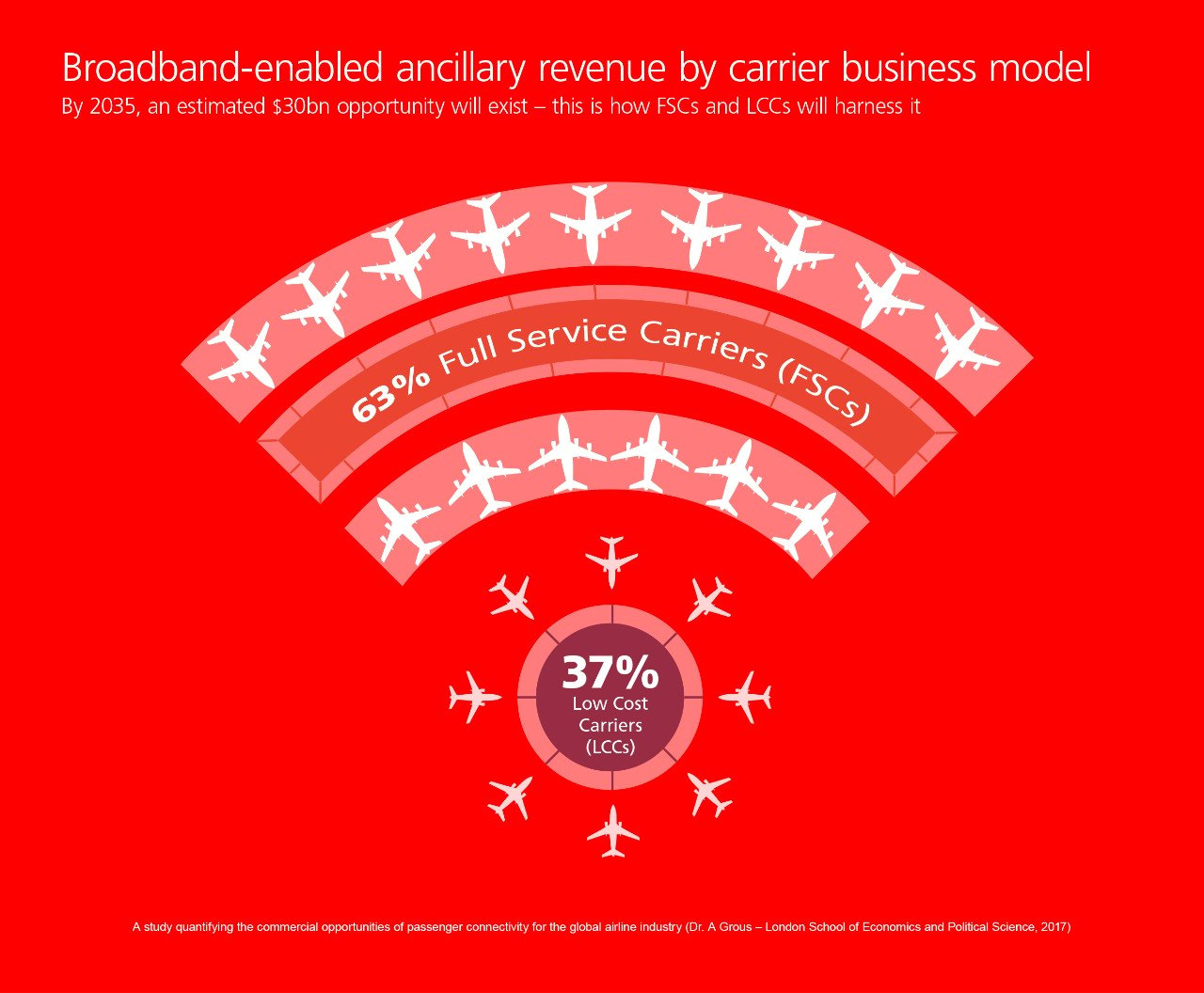

The study predicts the share of total ancillary revenue for full service carriers vs low cost carriers will stay more or less constant between 2018 and 2035, at roughly 2:1. This may seem counterintuitive, but the calculations are driven by FSC’s proportionately longer average flight times, giving passengers more hours to fill (and more time to spend money). Nonetheless, the study also recognises that the stronger retail mind-set of the low cost sector, experienced with à la carte pricing models, may lead to greater adaptability when it comes to implementing broadband-enabled services.

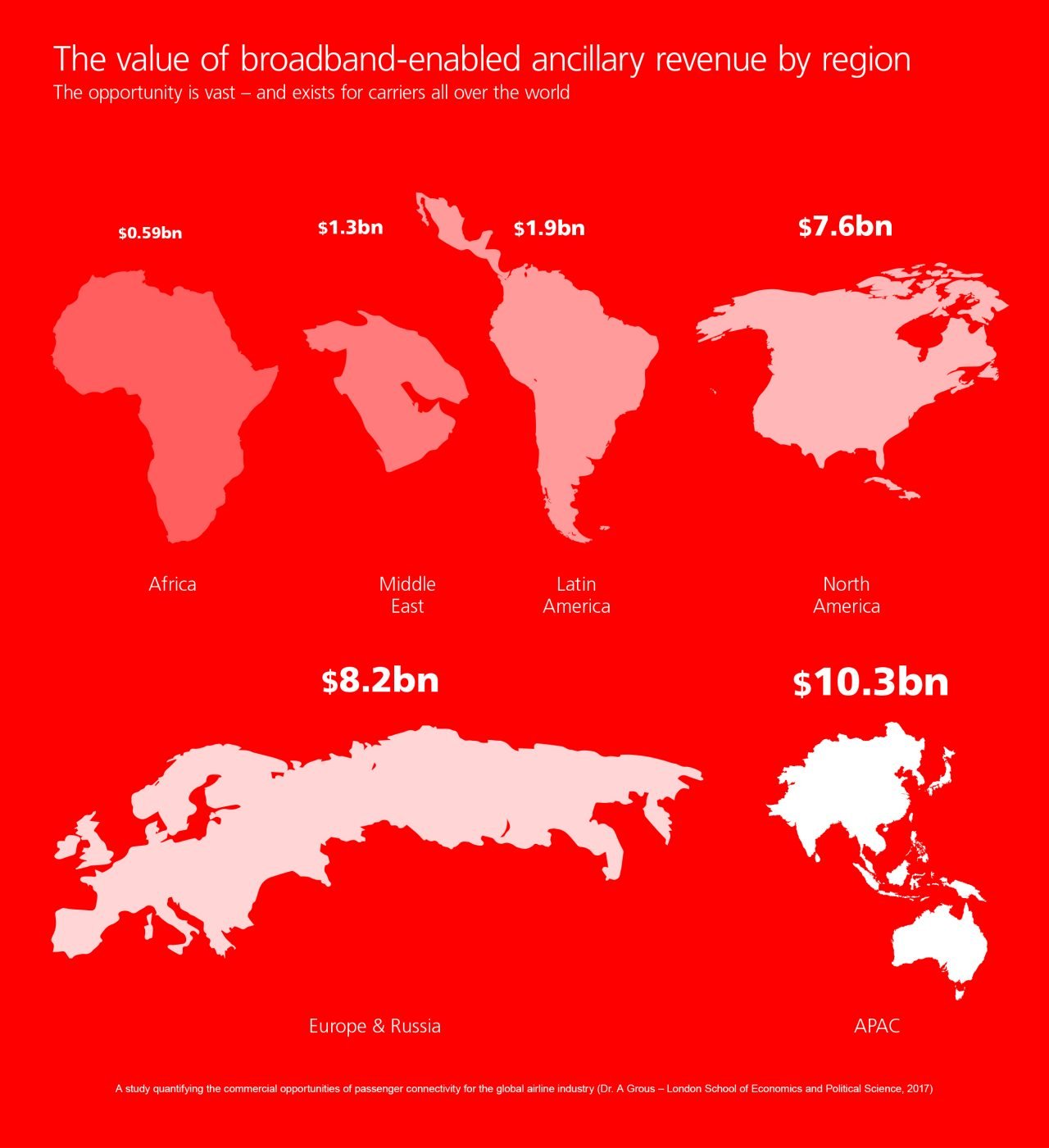

The regional revenue split is more varied. With IATA estimates for 3 bn passengers in the region by 2035, Asia Pacific is set to be the largest market for broadband-enabled ancillary revenue by then, valued at $10.3bn. Europe and North America follow, at $8.2bn and $7.6bn respectively, with Latin America, the Middle East and Africa at $1.9bn, $1.3bn and $0.58bn.

As airlines forge strong commercial relationships with suppliers of products, content and services to monetise passenger data, and align with new partners, they will unlock sizeable new revenues thanks to inflight connectivity.

In short, it’s a brave new world full of possibilities. In 2035, what will that overall broadband-enabled market worth $30bn look like, and who will be the major players? And what of the $130bn market within 20 years? Just as few could have envisaged how significantly a taxi app (Uber) or a home rental website (Airbnb) would change the private car hire or hospitality industries, we’re only now getting a sense of what connectivity-led digital transformation could mean for airlines.

“If airlines can provide a reliable broadband connection, it will be the catalyst for rolling out more creative advertising, content and e-commerce packages,” says Dr Grous. “We will see innovative deals struck, partnerships formed and business models fundamentally changed.”

With a revolution for ancillary revenue on the horizon and the requisite inflight broadband technology available today, there’s no time to lose – as Dr Grous states. “Broadband enabled ancillary revenue has the potential to shape a whole new market and it’s something airlines need to be planning for right now.”

This is the bottom line boost that the industry has been waiting for. This is the pivot point for the connectivity revolution.

Dr Alexander Grous is a lecturer at the Department of Media & Communications and Director of the research function for LSE Enterprise. He’s a specialist in demand-based modelling, communications and transport economics.

Private sector experience includes CXO level roles in mobile communications, high-technology, e-commerce, banking, FMCG and finance. He’s also held strategic roles in directly relevant organisations including Telstra and Lockheed Martin.